What Are The Basic Accounting Principles?

4 min read

Contents

- 1 Introduction

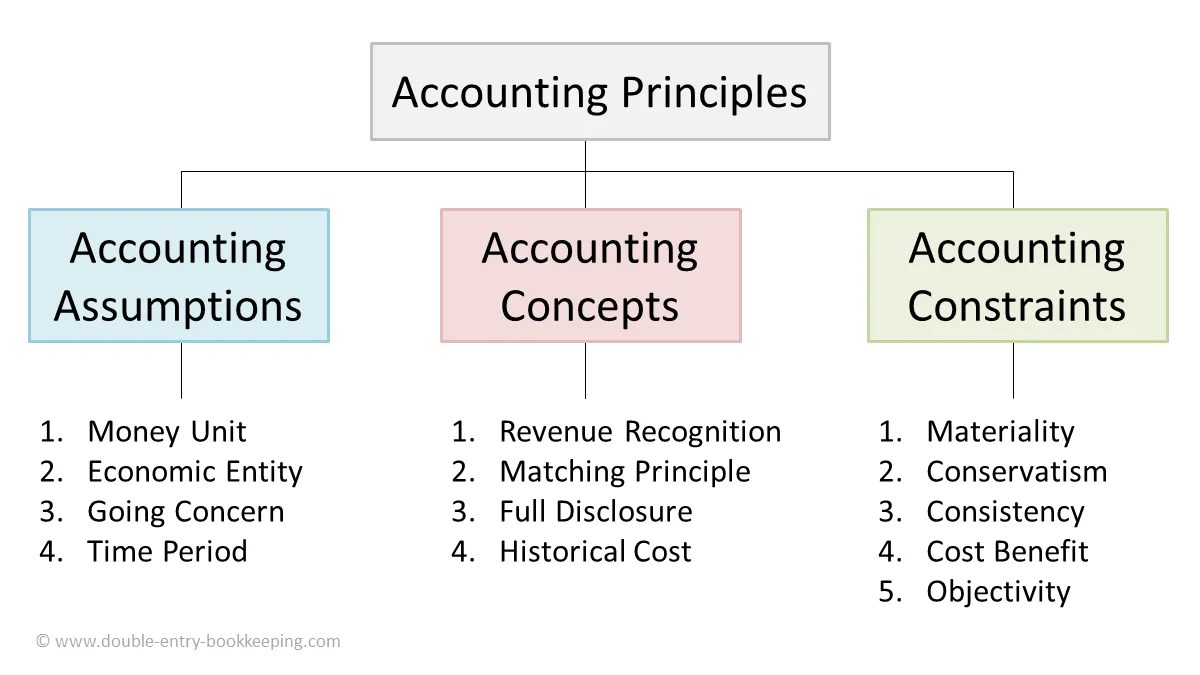

- 1.1 1. The Principle of Entity

- 1.2 2. The Principle of Going Concern

- 1.3 3. The Principle of Historical Cost

- 1.4 4. The Principle of Revenue Recognition

- 1.5 5. The Principle of Matching

- 1.6 6. The Principle of Consistency

- 1.7 7. The Principle of Materiality

- 1.8 8. The Principle of Objectivity

- 1.9 9. The Principle of Full Disclosure

- 1.10 10. The Principle of Conservatism

- 2 Conclusion

Introduction

Accounting principles are the foundation of any successful business. They provide a set of guidelines and rules that govern how financial transactions are recorded, analyzed, and reported. These principles ensure accuracy, consistency, and transparency in the financial statements, which is crucial for making informed business decisions.

1. The Principle of Entity

The principle of entity states that a business’s financial transactions should be kept separate from the personal transactions of its owners. This means that a business’s financial records should be maintained independently and not intermingled with the personal finances of its owners or employees. By following this principle, it becomes easier to track and understand the financial performance of the business.

2. The Principle of Going Concern

The principle of going concern assumes that a business will continue to operate for the foreseeable future. This means that the financial statements are prepared with the assumption that the business will not be liquidated or cease operations. It allows businesses to prepare financial statements that reflect the long-term outlook and sustainability of the business.

3. The Principle of Historical Cost

The principle of historical cost states that assets should be recorded at their original purchase cost, rather than their current market value. This principle ensures that the financial statements are based on objective and verifiable information, as the original purchase cost is more reliable and less subjective than market value estimates. It also provides a consistent basis for comparing financial information over time.

4. The Principle of Revenue Recognition

The principle of revenue recognition dictates when and how revenue should be recognized in the financial statements. It states that revenue should be recognized when it is earned, regardless of when the payment is received. This ensures that revenue is reported in the appropriate period and matches with the expenses incurred to generate that revenue. It prevents the manipulation of financial statements by delaying or accelerating the recognition of revenue.

5. The Principle of Matching

The principle of matching requires that expenses should be recognized in the same period as the revenue they help generate. This principle ensures that the financial statements accurately reflect the costs incurred in generating revenue. It helps to determine the true profitability of the business and prevents the misrepresentation of financial performance by deferring or accelerating the recognition of expenses.

6. The Principle of Consistency

The principle of consistency requires that the same accounting methods and principles should be used consistently from one period to another. This ensures comparability and reliability in the financial statements. Any changes in accounting policies or methods should be disclosed and justified, allowing users of the financial statements to understand and assess the impact of these changes.

7. The Principle of Materiality

The principle of materiality states that financial information should be disclosed if its omission or misstatement could influence the economic decisions of users. It allows businesses to focus on reporting information that is significant and relevant, rather than immaterial details. This principle helps to ensure that the financial statements are concise, yet informative and useful for decision-making.

8. The Principle of Objectivity

The principle of objectivity requires that financial transactions should be supported by objective evidence and verifiable documentation. It prevents the inclusion of subjective opinions or estimates in the financial statements. By following this principle, businesses can ensure that their financial information is reliable, accurate, and free from bias.

9. The Principle of Full Disclosure

The principle of full disclosure states that all relevant financial information should be disclosed in the financial statements, including any significant events, transactions, or contingencies. This allows users of the financial statements to have a complete and accurate understanding of the financial position and performance of the business. It helps to facilitate transparency and accountability.

10. The Principle of Conservatism

The principle of conservatism suggests that when there are uncertainties or doubts, businesses should err on the side of caution and choose the option that is least likely to overstate assets or income. This principle helps to prevent the overstatement of financial performance and ensures that the financial statements are more conservative and reliable.

Conclusion

Understanding the basic accounting principles is essential for maintaining accurate and reliable financial records. By following these principles, businesses can ensure transparency, consistency, and accuracy in their financial statements. This provides a solid foundation for making informed business decisions and building trust with stakeholders.